Debt is bad. But not always. In another blog post I discussed how I purchased a bargain property titled Bought a Bargain Property: Now What? using Investment Tip 1: Types of Bargain Properties. At first, I attempted to get a line of credit from my home to fund all my remodeling expenses for the new property. I got rejected. Not just once. Including the combined attempts by my wife and I, we got rejected a total of 7 times by different banks!!! We didn’t get rejected because we have bad credit. The reasons stemmed from income being too low or having too many loans on our properties. What saved the day? Credit cards.

If there is one thing I learned in life is that credit cards are not that bad even though yearly interest rates hover around 10%-25% for most cards. And there are beneficial methods to the madness of credit cards. But it has to be done the right way! I will go over the why and how below:

Cashback Credit Cards

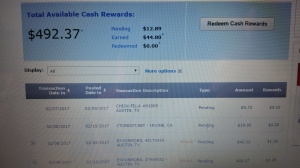

Credit cards pay me just for using them. Yes, no kidding! With my two rewards credit cards, the credit card companies PAY ME a total of about $600 to $1500 per year! If I include my wife’s returns from her credit card it is even more! Below is what I have earned so far in the past 7 months or so:

How does this work? Is there a method to the madness? Yes and here we go! Step one is to first acquire a credit card that offers the cashback option which are typically called Cash Rewards Credit Cards. And there are plenty online and at your local bank. Most Cash Rewards Credit Cards reward you 1%-3% of the amounts used depending on the purchase and terms of service. Step two is to use those credit cards for ALL your expenses and purchases whenever possible. This includes groceries, bills, gas, and more! Last step is the most important because this is how you make your money. Pay your credit cards before the credit card companies charge you interest. There is usually a grace period of about 21 days. Which means that if you pay before then, you get charged nothing, zero, nada! But guess what? The credit card companies now pays you! If the credit card is from the same bank from your checking account sometimes they give you even MORE money–up to 50% of your rewards amount! However, you must redeem your amount via transfer to your checking account instead of getting a check or immediate cash. That means if I was to redeem my $892 rewards by way of transfer to my checking account, the bank/credit card company will give me $446 more on top of the $892 already earned! A total of $1338! Is this madness? If it is, I am liking it.

Why do credit cards do this? The credit card companies are betting that you don’t pay them back on time and keep a balance on the card. The typical charge rate (about 10%-25%) is way higher than the rewards rate of only about 1%-3%. So if you hold a debt throughout the year, even if they give you 3% in rewards, they still make money because the charge rate will be 7-10 times higher. Also, when you don’t consistently pay within the 21 day window they charge you interest and their chances to make money increases. But if you pay before the charge window every time and do it the right way, you are the winner!

Cash Advance and Credit Card Limits

Cash Advance is having the option of drawing out a portion of your credit limit in CASH. Most credit cards have a cash advance option which is a little different from your credit card limit. Your credit card limit is the maximum amount you can use. Then you have a Cash Advance limit which is usually lower than the overall limit or equal to it. The interest rates for both are also different. For example, your credit card limit could be at 5000 at 12% and have a Cash Advance option of $1000 at 20% on the same card. Cash Advance interest rates are usually higher.

Many people think that having a high credit card limit is bad. It is not. Having very high credit card limits are beneficial in two ways. One, your credit score will go up when your debt ratio is low compared to your limit. As an example, if you have a limit of 5000 and owe $5000 you have reached your limit. Your debt to limit ratio will be high at 1/1 or at 100% which will affect your credit score negatively. Now let’s say your limit is at 25,000 and still owe the same amount of $5000. Now you are using just 1/5th of your limit, or only 20% of your limit as opposed to 100%. Your ratio is now considered low boosting up your credit score! Same debt, yet different results for your credit score!

How do you get a higher credit limit? Below are the steps:

Step 1: Call the customer service number on the back of your credit card.

Step 2: Say “I would like to request a higher credit card limit.”

Step 3: They will then ask you for the amount you want. I recommend you request double whatever your current limit is. For example if you currently have a 5000 limit ask for 10,000.

Step 4: They will then ask you for your current income, rent/mortgage information, and other minor information. They don’t verify this information. It is all verbatim. They are expecting you to be truthful in your discourse.

Step 4: They will run this information through a computer. There is a waiting period of about 5 minutes in most cases. Sometimes you will get what you requested and sometimes they come back with a different amount, usually higher than your current limit but lower than what was requested. Either way, your credit card limit is higher than before!

Step 5: Call every other month and do the same thing. Soon you will have limits that are very high. I have combined limits of about 70,000 spread out through my credit cards as an example.

How do you get a higher Cash Advance limit? Just follow the same steps except you request a higher Cash Advance limit. In fact, you could request higher limits for both at the same time. That is what I do for practicality.

Using the Cash Advance Option

The Cash Advance option is awesome to have! You will never know when you might need CASH. There are medical emergencies, death in the family, taxes due, property purchases, or in my case, for a remodeling project. But again, there is a method to getting the best deal on these advances.

Never accept the standard rate given for Cash Advances. Currently on one of my credit cards I have an interest rate of 18% if I draw out CASH. That is a lot of interest per year I will be paying, especially if I am drawing a large amount. What you do instead is call the number on the back of the credit card and ask for special promotions. They are usually way way better. The credit card companies equip the customer service representatives with these promotions to entice callers to draw out credit. Usually, people deny these requests because they don’t need or want it. What happens when you do want it? Well you call and find out what they can offer?

My Scenario with Cash Advance from a Credit Card

Again, I have an 18% rate if I draw out cash on that one credit card. I called the number on the back and asked for promotions for drawing out $20,000 in CASH. They put me on hold. The representative came back and offered me a draw out fee of 3% with no interest charged for an entire year! That means I am paying only 3%, which is the rate of inflation, on the money borrowed compared to the 18% if I didn’t call! Of course, after the year is up I will be paying the going rate of 18% but I have one whole year to pay it all back. I drew out a combined $60,000 CASH with the same 3% draw out fee from three credit cards for the remodel. I have one year to pay it all back before the high interest kicks in and that is the goal. The numbers have been run and it could be done.

To sum it all up, credit cards are not so bad. There is some method to the credit card madness.

You clearly know your credit cards! You’re right, there is an art to using them and they really aren’t bad if you use them right. Just make sure you pay them back before the interest gets charged.

I liked the bit about ringing up to up your credit limit, it’s really helpful as it isn’t something I’ve done before and I’ve always worried about messing up my credit rating.

LikeLiked by 1 person

I recommend you up that credit limit! It could only help! And there is nothing to lose by trying..only gain.

LikeLiked by 1 person

I never thought about the “debt to limit ratio”. Do you have any information as to what point is your borrowing rate too high or does that ever happen? I’m in Canada in case our credit score “rules” are different.

Looking forward to reading more.

Besos Sarah.

LikeLike

Hi Sarah, here in the US to have a more positive effect on your credit score, the debt to limit ratio should be about 30% or below…the higher the ratio from that point the more likely it would be detrimental…hope that helped in any way possible. Besos de regreso

LikeLike